If you have a mortgage, you are being charged interest by the bank each month. To gauge how much this is, most loans that are standard terms from 25 to 30 years. It will mean you pay off twice what you borrowed. So, your repayments over time amount to ~ 50% interest and 50% principal.

As you make your regular weekly, fortnightly or monthly payments you’re paying off a bit of what you owe, which reduces the amount of interest you will be charged. When you do the calculation at the bank, they tell you an amount you will pay each month, every month, until the loan is discharged. It’s a regular payment, always of the same amount.

But that’s not how the interest is charged – it is not linear. You’re charged most of the interest in the first 10 years of your 25-30 year loan, during which time the principal (the amount you owe) remains depressingly high. But soon enough the scale tips, and you are paying off decent amounts of principal and the interest charged is dropping. It is in your interest to reduce that interest charged as soon as you can, especially on your home loan as this has no tax benefits.

Best options for mortgage repayment

Ways to reduce the interest you pay: There are three options to pay less than the amount of interest due on the full term of your loan:

- Pay more than your minimum monthly repayment,

- Pay off a lump sum, or

- Use an offset account.

Method #1: Pay more than minimum repayments

One slow-and-steady way to reduce the interest you are charged is to add more to your regular payment. An extra $10 or an extra $1,000 on top of your minimum repayment has the same directional effect: less interest charged and paying off the loan quicker. It’s just a matter of scale: the more you pay, the quicker the loan comes down. This has an effect on cash flow. You have to find that $10 or $1,000 (or whatever it is for you) from your current income.

Another subset of this option is to switch to fortnightly repayments that are half the value of monthly repayment. This is like making 13 monthly repayments in the year instead of 12. It’s my favourite sneaky way to get ahead on mortgage payments.

Method #2: Pay off a lump sum

Sometimes you may find yourself with a chunk of change in the order of thousands of dollars. Perhaps you sell a toy (e.g. jet ski, boat), or you get a bonus at work, or you get some inheritance. You could use that chunk to pay off a part of your mortgage in what’s called a lump sum payment. This reduces what you owe, and therefore the interest you’re charged. Because the time period of the loan remains the same but the amount you owe is less, the minimum repayment required drops.

You could then do one of two things:

- Keep making the same repayments, which then becomes like method #1 as you’re effectively paying more than minimum, or

- Ask the bank to reassess your payment for the new amount, dropping your repayments to the new minimum.

Option 1 results in the least amount of interest charged.

Method #3: Put the lump sum in an offset account

Instead of paying off some of the balance of your mortgage, you could ask your bank to set up an offset account. This is a savings account linked to your mortgage. As the name implies, it offsets the balance on your mortgage and you are only charged interest on the difference between the two.

For example:

- Your mortgage balance is $300,000

- Your offset balance is $100,000

- You are only charged interest on $200,000 instead of being charged interest on $300,000

The difference between the loan amount and the offset balance. With an offset account, the loan balance stays the same so the minimum repayments do too. It is just that you are charged less interest, so the loan balance goes down quicker as more of your repayment goes to the principal.

So, which is better?

There is no right or wrong here. There is only what works for you, in your personal circumstances, at this point in your life. Here is my quick guide to making this decision:

If you do not have a lump sum saved somewhere, just forget the offset and concentrate on upping your regular repayment by a few bucks at a time. But another advice is you really should have a lump sum somewhere. It is a nice cushy buffer fund to cushion you through the inevitable shocks of life. Time to get started on that.

If you do have a lump sum, answer these two questions:

- Can I comfortably keep making my repayments at this rate? If not, paying off a lump sum will help drop your repayments.

- Do I think I might want to access this money again? If yes, you may prefer an offset.

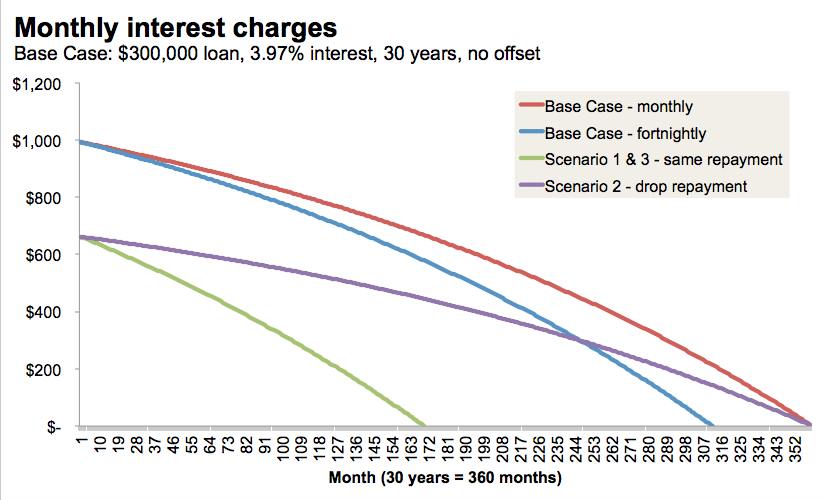

To help you get your head around what happens with the interest, here’s a chart showing a few different scenarios:

- Red line: Base case with loan $300,000, rate 3.97%, term 30 years, monthly repayment $1,427.06

- Blue line: Method 1, pay off a bit more, repayement $714 per fortnight.

- Green line: Combination of Method 2 part 1 and Method 3, pay off $100,000 and keep same repayments OR put $100,000 in offset , repayments remain $714 per fortnight

- Purple line: Method 2 part 2, pay off $100,000 and drop to minimum repayment , repayments drop to $951 per month, same term 30 years

Standard home loan terms

| Summary | Start | Loan | Interest | Years | Offset Acc | Maturity | |

| Loan | 01-Jan-23 | $300,000.00 | 3.97% | 30 | $100,000.00 | 31-Dec-52 |

Time and money savings between 3 options of repayment

| # | Repayment | Last Payment | Repay | Total Repay | $ Saving | Months Savings | Years Savings |

| A | Monhtly | 31-Dec-52 | $1,427.06 | $513,742.98 | Based / Default Scenario | ||

| B | Fortnightly | 19-Sep-48 | $714.00 | $478,913.78 | $34,829.20 | 51 | 4.3 |

| C | Weekly | 12-Sep-48 | $357.00 | $478,423.95 | $35,319.03 | 52 | 4.3 |

| D | Offset & Fornightly | 27-Dec-36 | $179.00 | $211,561.31 | $302,181.67 | 192 | 16.0 |

I also designed the worksheets for you to workout your own term loan.

Homecoze